The programme Next Generation EU (NGEU) is designed to speed up the EU recovery and spur growth over the medium and long term. More importantly, says Apostolos Thomadakis, it represents a unique opportunity to lay the foundations of a deep and liquid European safe asset. The EU is fast becoming a major player on the capital markets and a major provider of safe assets in euros, thereby reinforcing the international role of the euro. The funding of a considerable part of NGEU by green bonds, means that the EU – as a leader in green bonds issuance – will manage the largest green bond scheme in the world. For the first time ever, through NGEU there is an inherent fiscal stabilization effect for the EU budget.

A bit more than ten years ago, in response to the European sovereign debt crisis, the newly established European Stability Mechanism (ESM) had – at that time – a lending capacity of EUR 60 billion. Alongside that, the European Financial Stability Facility (EFSF) was equipped with an additional EUR 400 billion, bringing the combined firewall to about EUR 500 billion. In 2020, the EU had in total EUR 800 billion of safe assets (i.e. the European Commission [EC] issuance, the ESM Pandemic Crisis Support, and the European Investment Bank [EIB] financing), which is estimated to reach almost EUR 2 trillion over the coming years. Adding the double-A and triple-A issuers, such as Germany and the Netherlands, issuance of European safe assets can be at the range of EUR 5-5.5 trillion. However, this is still not enough. The US has about 90% of GDP in safe assets, compared to Europe’s 40% of GDP.

In order to be able to overcome different crises, different tools are needed. The current pandemic has hit countries very symmetrically, as opposed to the global financial crisis, where the impact was more heterogenous across countries. Whereas for the latter – where reforms and restructuring were needed – the ESM toolkit proved to be very useful, Covid-19 requires a very different approach. Having an EU-27 blended bond like the one offered under the Next Generation EU (NGEU) programme, represents a unique opportunity to lay the foundations for a truly European safe asset. NGEU borrowing will be used up for loans and, for the first time, to finance grants.

In the context of the NGEU, the EC is acting like a de facto sovereign issuer. This requires building a primary dealer network with 42 banks, launching the EU-Bill programme, starting bond auctions, maintaining a regular communication with investors through funding plans, engaging with Member States and debt management offices (DMOs), as well as trying to broaden the investor base to reach investors across the world (13% of SURE bonds are sold to overseas investors, and about 10% of the NGEU bonds). The aim is to set the EU on the path as the benchmark green bond issuer and to build a liquid curve from 5 to 30 years.

One very important difference with a sovereign issuer who has rolling financing needs, is that the EC issues debt for very delineate policies. Having said that, there are two important consequences. First, issuance is very closely linked to what the expenditure needs of the European economy are – both in terms of timelines and amount. Second, debt issuance is limited and it will cease in 2026 for the NGEU. Whether this will prevent the EU from achieving similar liquidity to that of France and Germany, remains to be seen. However, refinancing could go beyond 2026 for another ten years, up until 2036.

The EC has gone to the market to fund very identifiable social and economic recovery needs, by also adding asustainability twist to the process. Thus, the issuance of EU debt can take place without crowding out Member States, given that the Commission is funding complementary needs at a different level of government.

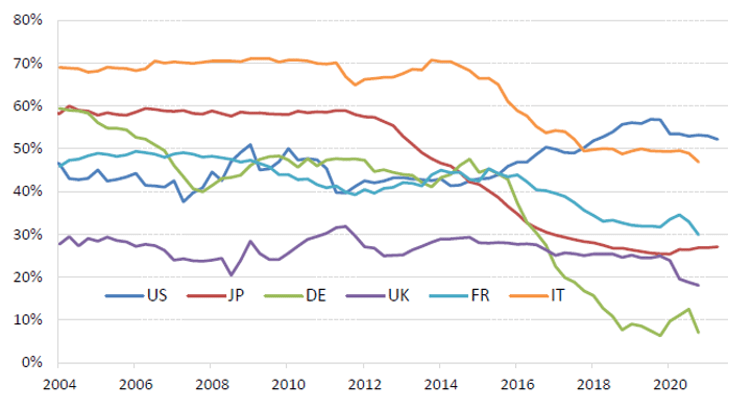

From the market side there is a huge appetite for highly liquid and highly rated EU debt. This is evident from the high levels of oversubscription (over 11 times) for both NGEU and SURE (Support to mitigate Unemployment Risks in an Emergency) transactions. Factors such as the search for safety, the scarcity of safe assets, and collateral needs contribute to this demand. For example, with regards to the scarcity of safe assets, there is only around 10% of German debt that is actually available to all investors (Figure 1). Having an EU safe asset would contribute towards reducing this scarcity. But also in terms of liquidity, the EU’s debt is now on a par with that of sovereigns, a big shift compared to where Europe was pre-pandemic.

Borrowing from the markets can be a useful component of the EU budget, particularly in dealing with longer-term funding needs. The EU budget remains small as a percentage of GDP (at around 1% of the EU’s total GDP). However, by augmenting it with an additional amount of borrowing of up to 0.6% GDP per year, the borrowing under NGEU can have a real impact on the EU as a whole.

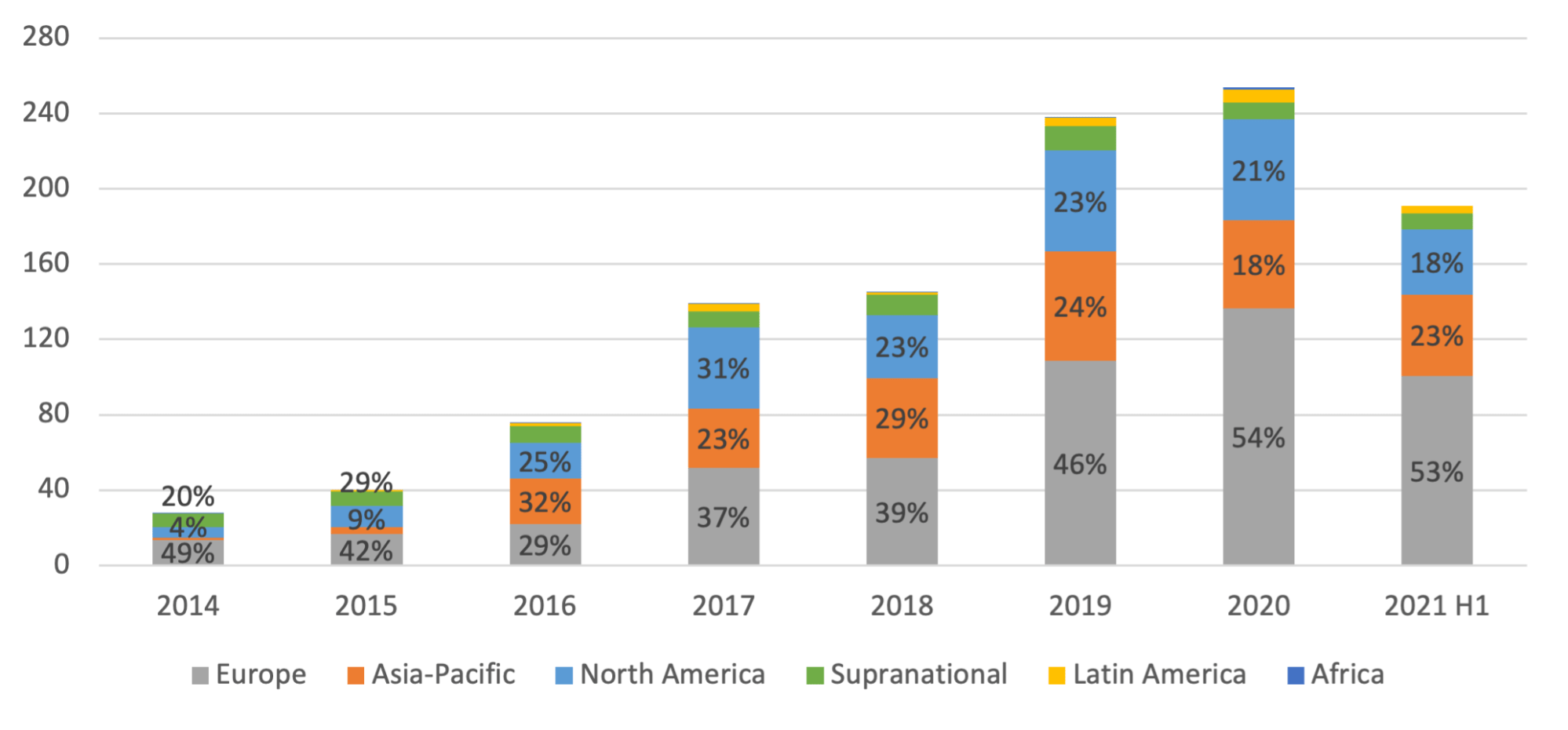

Something that should not be neglected, given that Europe wants to establish itself as a leader in green bonds, is the fact that about 30% of the EU debt is green. In terms of year-to-date issuance of ESG bonds, Europe is leading the way accounting for over half of the global issuance (Figure 2). In addition, 60% of that is accounted for by sovereign governments or sovereign and supranational issuers.

With the NGEU green bond programme, Member States have allocated in excess of EUR 240 billion of their spending to climate related expenditures. This amount will be monitored regularly by the EC in order to ensure that the use of proceeds finance or refinance projects that are aligned with the taxonomy regulation. Thus, disclosure and impact reporting are crucial elements of it. However, there are some expenditures like climate research, social skilling, upscaling for which the climate taxonomy does not cater for. So there may be things that governments are spending money on that are not catered for in the taxonomy.

Finally, the Commission’s issuance programme also has spin-off benefits in terms of enhanced international capital market recognition of the euro. The EU can offer international investors an instrument that they can trust and trade in and out of for diversification purposes. For the first time through NGEU there is an inherent fiscal stabilisation effect for the EU budget. This itself has helped to avoid flight to safety at the beginning of the crisis and kept interest rates in a very narrow path. Moreover, the EU’s debt issuance is not going to break the sovereign doom loop in and of itself. But is an alternative tool to sovereign debt issuance. Overall, the diversification away from domestic sovereigns strengthens the bank balances.

Dr Apostolos Thomadakis is Researcher at the European Capital Markets Institute (ECMI), an independent research institute run by the Centre for European Policy Studies (CEPS).

This piece builds upon discussions held during the European Capital Markets Institute (ECMI) Annual Conference on 30 November 2021.

Note: The views expressed in this post are those of the author, and not of the UCL European Institute, nor of UCL.

Featured photo by Ibrahim Boran on Unsplash.

Leave a comment